Saving money can feel like a major hurdle for individuals in the middle class. It often feels as if the paycheck vanishes before you realize it. Balancing the bills and attempting to savor life a bit, there’s scarcely anything remaining.

I faced this obstacle as well. Then, I stumbled upon something intriguing: simply by discontinuing subscriptions we seldom use, an average American can conserve a substantial amount each year.

So, I dedicated some time to research further and pinpoint practical methods to retain more money in our wallets. This post is centered on imparting those straightforward yet influential tips to my middle class peers.

We are discussing minor adjustments that generate a significant difference over time.

You will learn how to prioritize your own savings, find additional income effortlessly, and observe your wealth accumulate securely. Excited? Let’s begin.

Essential Money-Saving Strategies for the Middle Class

Saving money might seem hard, but it’s possible with some smart moves. I keep my costs down by cooking more at home and cutting out things I don’t use much, like some digital TV services or gym memberships that just collect dust.

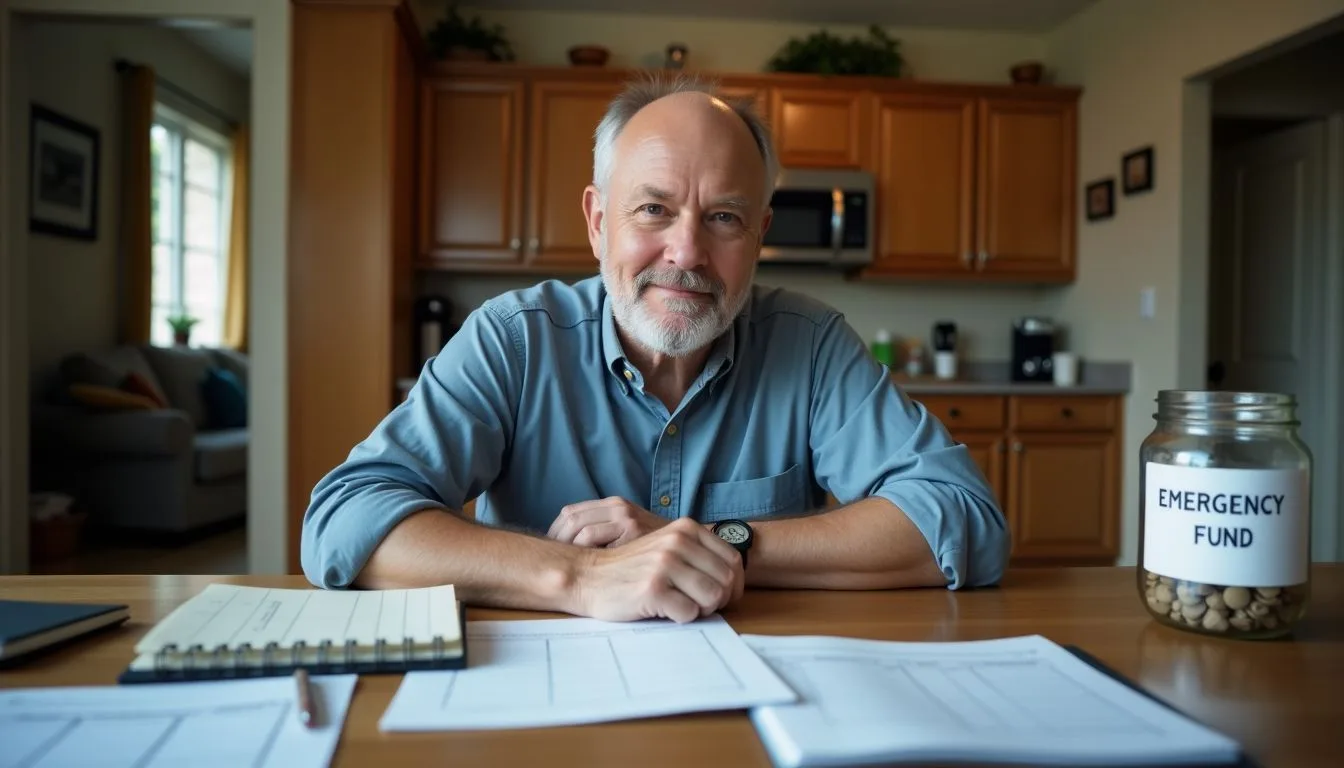

Establish an Emergency Savings Fund

I always make sure to set money aside for an emergency fund. This is a big deal for financial stability. For families in the middle class, it’s key to have savings ready for unexpected costs.

I stick to basic strategies like making a budget, cutting out things we don’t need, and hunting for discounts.

Each month, putting a little bit of money into the emergency fund helps it grow over time. I use financial apps to keep track of how much we save and what we spend our money on. This approach has made managing personal finances easier and less stressful.

Prepare Home-Cooked Meals to Cut Costs

Cooking at home saves a lot of money. It also means eating healthier. Here are ways to cut costs by making meals at home:

- Meal planning reduces trips to the store. This saves both time and gas.

- Buying ingredients in large amounts is cheaper. Stores offer discounts for bulk purchases.

- Cooking larger portions allows for leftovers. These can be lunches for the next day.

- Homemade meals cost less than eating out. Fast food adds up quickly over a month.

- Using coupons and looking for sales lowers grocery bills. Many stores have weekly specials.

- Growing vegetables at home cuts down on produce costs. Even small gardens help.

- Learning to cook different meals keeps things interesting. There’s no need to get bored with your food.

Next, let’s talk about evaluating and trimming unused subscriptions to save more money.

Evaluate and Trim Unused Subscriptions

After learning about cutting costs with home-cooked meals, let’s talk about another smart way to save money. This involves checking on subscriptions we don’t use much.

- I look over my monthly expenses. This includes everything from streaming services to gym memberships.

- Next, I note which services I haven’t used in the last month.

- I think about which subscriptions are really worth it for me and my family.

- Then, I cancel all the subscriptions we don’t use or need.

- Sometimes, I call the subscription companies. I ask if they can offer me a better deal or a discount.

- Every few months, I do this check again. It helps to keep my bills low.

- I also talk to friends and see what services they use and love. This gives me ideas on what might be worth keeping.

- Before signing up for any new subscription, I think twice if it’s something we truly need.

- If possible, I choose yearly payments over monthly for subscriptions we keep. They often come cheaper this way.

- Lastly, I keep track of all active subscriptions in a spreadsheet so nothing slips by unnoticed.

This simple task of reviewing our subscriptions helps us save a lot of money each year!

Long-Term Financial Planning Techniques

Looking ahead, planning for the future is key. This means setting sights on long-term money goals and finding smart ways to reach them. One way is by putting money into low-cost index funds—a choice many savers make because it spreads out their risk and can grow over time without much hassle.

Also, it’s important to keep check on lifestyle spending as income goes up; this helps in saving more rather than spending more. These steps are not just about saving but building a stronger financial foundation for years to come.

Invest in Affordable Index Funds

I put money into affordable index funds as part of my financial plan. These funds are a smart choice for people like us in the middle class. They don’t cost much and help us spread our investments across many companies.

This means we don’t have all our eggs in one basket, making it safer over time.

Index funds come with low fees too. Less money goes to fund managers, so more stays in my pocket. It’s a way to build wealth without paying too much attention every day. I see it as setting up a foundation for a secure future, step by step.

Prevent Lifestyle Creep

Saving more money is hard if we keep spending more as we earn more. This habit, known as lifestyle creep, can hurt our financial goals. To fight this, it’s smart to set a budget and stick to it.

We should focus on what we truly need versus what we want. It helps to automate savings too. That way, a part of every paycheck goes straight into a savings account or an investment like index funds before we even see it.

The Oracle of Omaha once said:

Do not save what is left after spending; spend what is left after saving.

This advice makes us think twice about buying things that aren’t necessary. Instead of upgrading the car or moving into a bigger home right away when getting a raise, pausing and considering if these decisions help reach long-term financial goals matters most.

Keeping an eye on monthly expenses, especially on repeat charges like streaming services or gym memberships that are not used often, can also prevent unnecessary spending increases.

By choosing frugal habits over flashy ones and investing in options with good returns like mutual funds or health savings accounts instead of splurging, building wealth becomes easier.

Advantages of Money-Saving Practices

Saving money wisely leads to financial security. This means less stress about cash. Plus, it opens doors to more chances for growing your wealth. With a good savings plan, you can put cash into investments that grow over time.

You’ll be ready for emergencies too, without needing high-interest loans or credit cards. Smart saving also helps in cutting down on unnecessary monthly costs, like those gym memberships you never use or streaming services you rarely watch.

By focusing more on your spending and where your money goes each month, you gain control over your finances. In turn, this discipline extends to other areas of life, making budgeting for holidays and fun activities easier and guilt-free since you’ve planned for them.

In short, adopting frugal habits doesn’t just pad your wallet—it sets the stage for a richer life experience beyond just the dollars saved.

Achieve Financial Security and Lower Stress

I focus on financial prudence for peace of mind and less anxiety. Through sensible money management, I pave a smoother path for the future. I ensure the existence of a contingency fund.

Thus, in case of unforeseen incidents, the stress related to money sourcing can be avoided.

Allocating resources to straightforward avenues like index funds is also beneficial. It augments my savings without requiring me to hire external aid for financial handling. This strategy streamlines life and induces tranquillity, eliminating constant worries about bill payments or unexpected costs.

By diligently monitoring my monthly expenditures, from vehicle insurance to eating-out expenses, every saved dollar is a stride achieving financial autonomy and reducing stress for me.

Enhance Investment Opportunities

Preserving wealth assists me in considering improved investment alternatives. By amassing a significant amount, I can invest in offerings such as index funds that are championed by Warren Buffett.

These are typically less expensive and frequently yield advantageous returns over an extended period. Eschewing unnecessary purchases results in more funds available for allocation to investment opportunities where my money can appreciate.

Improved saving practices also encourage more informed choices regarding auto insurance and credit card rewards. Once my emergency reserve is robust, I feel confident reviewing possibilities such as certificates of deposit or even pursuing a secondary source of income.

In this regard, saving provides a safety net during challenging periods and reveals avenues to augment my resources through judicious investments.

Conclusion

Saving money can feel tough, but I found some ways to make it easier. First off, setting up an emergency fund gives peace of mind. Cooking at home and cutting unused subscriptions also keep more cash in my pocket.

Investing a little in index funds and avoiding lifestyle upgrades help grow savings over time. These steps lead to less stress and open new chances to use my money.

I see how these methods work well for anyone willing to try them. They’re simple and don’t take much time to start seeing results. This approach has taught me the importance of small changes for long-term benefits.

For those looking further into saving, exploring things like high-yield savings accounts or learning about tax breaks makes a big difference.

Let’s not wait to get better at managing our finances. Every step taken today builds a stronger tomorrow — financially speaking.